Every so often a client asks us some version of the same question: "What am I actually paying you for?"

I love that question. If you can't say plainly what you're getting for your money, you shouldn't be paying for it. So let me answer it honestly, the way I would across the table from you.

I think about the value we provide in three buckets. The first you can see. The second is real but invisible. The third you won't fully appreciate until decades from now, when it's too late to go back and buy it.

The value you can see

Start with the obvious: your portfolio and what it returns. The only number that matters here is your net return, what you actually keep after fees. Not gross. Net.

This is where people get the fee conversation backwards. They compare a 1% fee to a 0.25% fee and feel clever for noticing. But fees are already baked into net returns:

11% gross − 1% fee = 10% net

3.75% gross − 0.25% fee = 3.5% net

Which one do you want? Nobody eats "the fee I saved." You eat what's left. A higher fee that delivers a higher net result is the cheaper option, every time.

Curious what a fee actually costs you over decades? Run your own numbers in the Advisor Cost Calculator →

But how is a higher net number built? Not with a hot hand or luck. With a diversified portfolio, invested systematically, run by disciplined rules rather than mood, so it doesn't chase greed when markets are euphoric or flinch in fear when they fall. The proof is what happens without it. DALBAR has measured this for decades, and the average investor earns far less than the very funds they hold, often by several percent a year, because, left alone, people buy high, sell low, and move at exactly the wrong moments. The market didn't shortchange them. Their own decisions did.

People misjudge activity, too. There's a stubborn myth that a good advisor is a busy one. The data says the opposite. Over 20+ years, passive investing beats active more than 99% of the time, and you can't identify that lucky 1% in advance. Just trying to find it makes you do worse.

So yes, sometimes the most valuable thing I do is nothing. But "doing nothing" on purpose, while the news screams and your gut begs you to act, isn't laziness. It's the hardest discipline in this business, and it's a strategy. One that only works with a good plan underneath it.

The value that's real but invisible

Here's the part that never shows up on a statement.

Vanguard studied this for years and gave it a name: Advisor's Alpha. Their finding is that a good advisor can add up to, or even exceed, 3% a year in net returns. Not every year, but concentrated exactly when it matters most: during euphoria and during panic.

The single biggest piece of that 3% isn't clever stock-picking. It's behavioral coaching. Vanguard puts its value anywhere from zero to over 2% a year. In plain terms, it's me talking you out of the mistake you were about to make.

This is the value of the negatives that never happen. Keep you from selling at the bottom in a panic, or from piling into a hot trend right before it reverses, and the loss simply never happens. Flag the unnecessary tax bill before you pay it. Trim the concentrated position before it becomes the risk that sinks you. None of it shows up on a statement, because the whole point is that it never occurred. Yet avoiding a single panic sell in a bad year can be worth a 20 to 40% swing, as real as money in your pocket.

The rest of that 3% comes from the unglamorous, repeatable work: low-cost diversified funds, rebalancing so you're not carrying risk you never agreed to, and tax-smart moves made at the right time. Add global diversification and real dollar exposure, and you have value that's quiet but compounds.

The value you can't put a number on

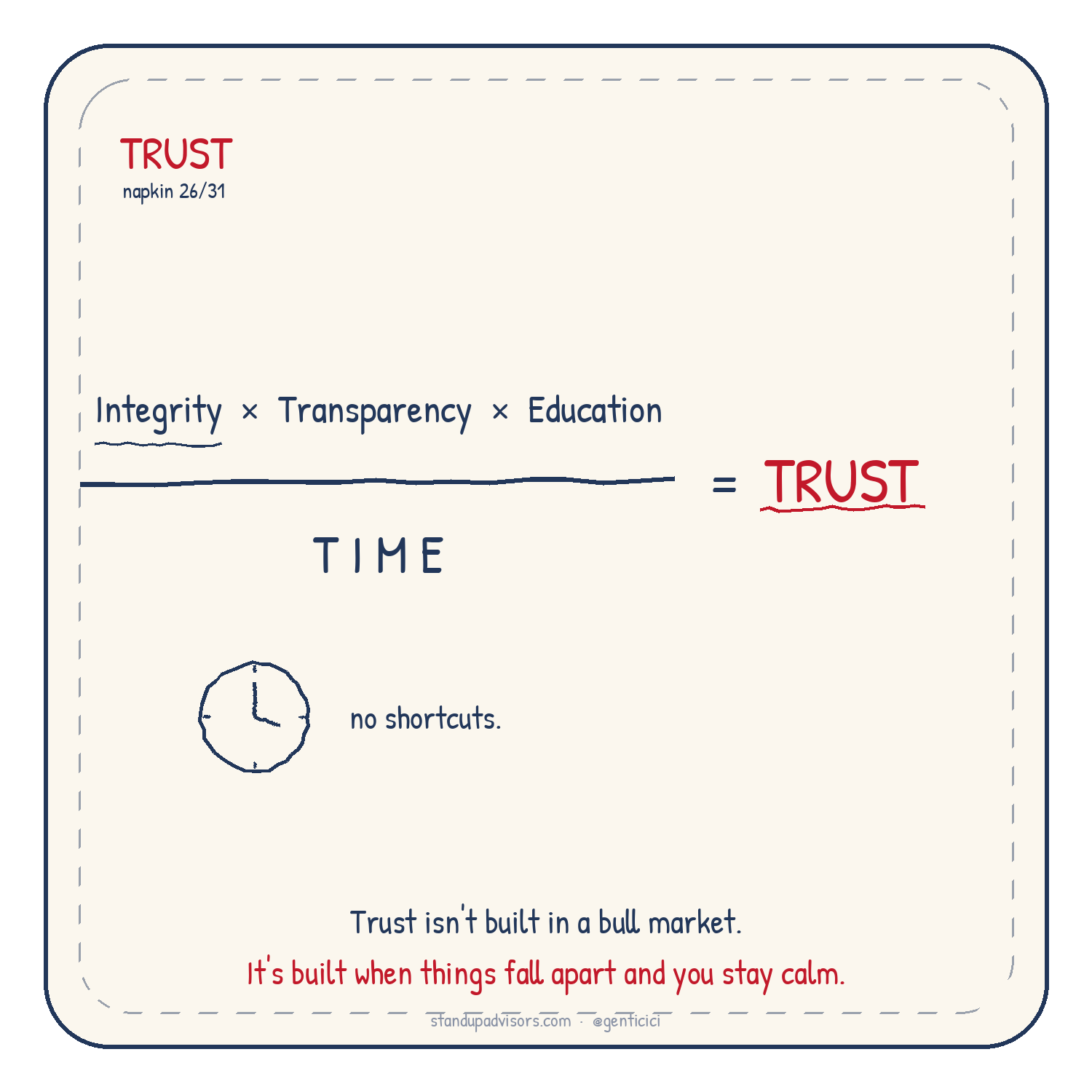

The third bucket is the hardest to measure and often the most important: one person who sees the whole picture, and how every piece connects.

Most financial lives are a drawer full of parts nobody is coordinating. An account here, an insurance policy there, a tax preparer who never speaks to whoever manages the investments, a 401(k) on autopilot. Each piece can be fine on its own and still, uncoordinated, leave money and peace of mind on the table.

Comprehensive planning is the opposite. It's one mind holding all of it at once: your investments, taxes, cash flow, risk, and the timing of the big decisions, all pointed at the life you actually want them to fund. The value isn't in any single piece. It's in how they fit together, so a move in one corner doesn't quietly cost you in another, and every part is pulling in the same direction.

And it's held by someone unbiased, who charges you directly and owes you nothing else. No product to sell, no quota, no hidden incentive. Just someone disciplined and unemotional on your side of the table, who knows your whole situation and tells you the truth, year after year.

You can't put that on a statement. Having one trusted person see the entire board, and stay steady when you can't, isn't expensive. Over a lifetime, it's priceless.

What about AI?

I'd be dodging the obvious if I didn't address it. AI is here, it's powerful, and it will keep getting better at the mechanical parts of money: running numbers, screening funds, flagging tax moves. Good. I welcome it.

But notice which bucket AI is great at: the visible one, the part that was already getting commoditized. The rest takes someone who knows you, not just your account.

Here's the part most people miss. The narrower and deeper the expertise, the easier it is to encode and master. What it struggles with is the opposite: the generalist. My job isn't to know one thing to the bottom, it's to see how all of it fits together for one person: your investments, taxes, cash flow, risk, career, and the life you actually want. That breadth, paired with a real relationship and the read on when you're about to act out of fear or greed, is what a narrow tool can't replicate.

So the best advisors won't compete with AI. We'll use it, letting it automate the low-value tasks so we can spend more time on the high-value ones: understanding you, managing expectations, and being human when it counts.

That's the job. That's what you're paying for. And it's the part that only gets more valuable as everything else gets automated.

As always, if you want to talk through any of this, our door is open.

— Genti

Genti Cici, CFP®, CAIA · Founder, StandUP Advisors